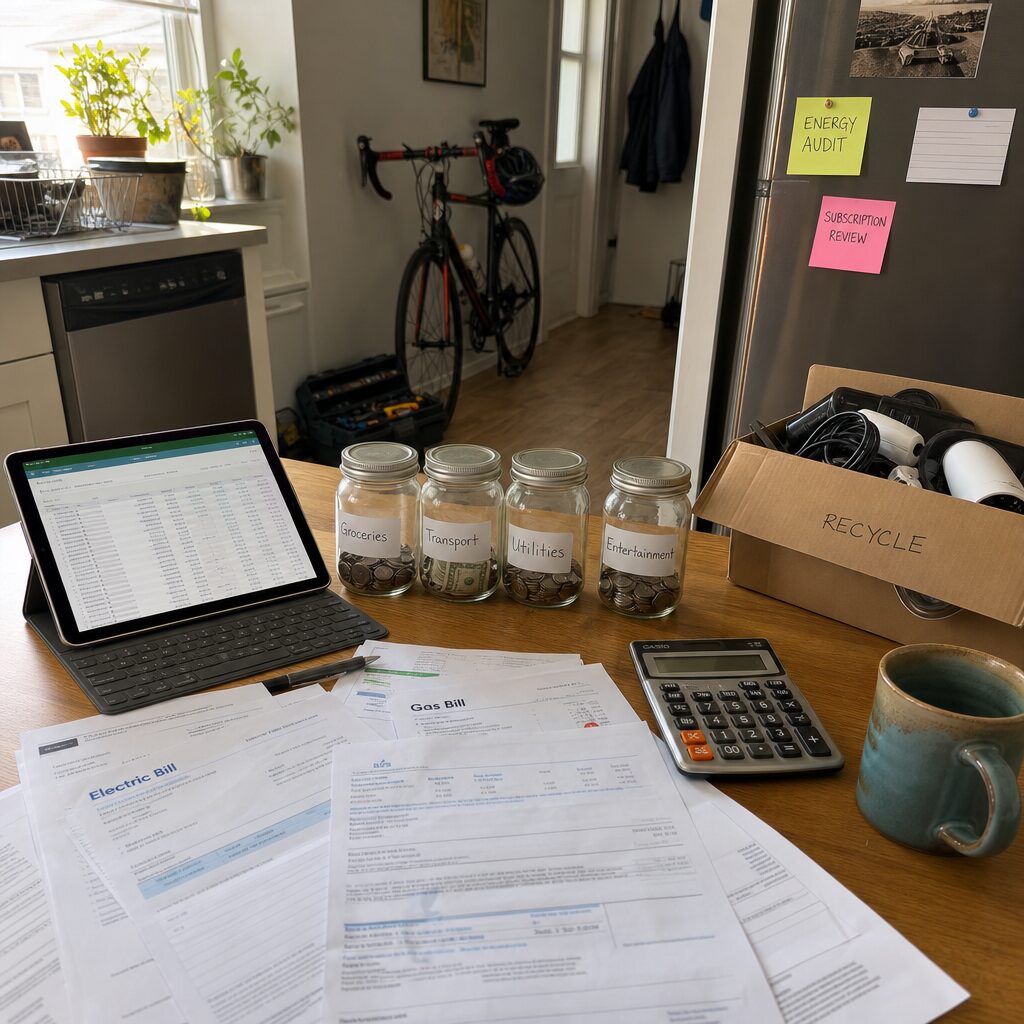

When Your Subscription Audit Becomes Passive — Time to Replace Auto-Renew Habits

Most households start saving by cancelling unused subscriptions or consolidating streaming services. A sign it’s time to upgrade that tactic is when you can no longer remember what you subscribed to or you stop reviewing bank statements for recurring charges. If your monthly list is a blur, the initial savings tactic has decayed into passive neglect and may actually cost you more through overlapping services.

Upgrade by adopting a single, visible subscription map: a simple spreadsheet, an app that tracks recurring payments, or a monthly calendar reminder to review charges. Replace ad-hoc cancellations with rules—annual review dates, thresholds for price per use, and a ‘one-in, one-out’ rule for entertainment services—to prevent drift back into waste.

When Energy Hacks Aren’t Working — Replace One-Off Thermostat Tricks

Many people save on bills with simple energy hacks: turning down the thermostat, using LED bulbs, or unplugging chargers. These are useful, but a tell‑tale sign they need upgrading is stagnating energy usage despite continuing the same habits. If bills plateau or climb during the season, the marginal benefit of those hacks has been exhausted.

Consider swapping single-point habits for systemic upgrades: smart thermostats, zoned heating, cavity wall insulation or a professional energy audit. These require upfront spend but deliver consistent monthly savings and stop the need for daily micromanagement. Think of the upgrade as moving from manual coin‑counting to an automated machine that prevents leakages you can’t see.

When Grocery Savings Kill Joy — Replace Extreme Couponing with Strategy

Couponing, batch cooking and bulk buying are classic monthly savings moves. However, when you find shelves of food going out of date, repetitive meals draining morale, or you’re spending hours hunting deals with negligible savings, it’s time to evolve the approach.

Replace time‑intensive deal-chasing with a value-oriented grocery strategy: price-per-unit tracking, flexible meal plans built around loss-leader items, and a rotating pantry system to reduce waste. Combine occasional bulk buys for staples with fresher, weekly purchases for perishables. The objective is to keep savings while restoring variety, nutrition and time.

When Your Commute Savings Backfire — Replace the Car-Only Mindset

Saving on transport by driving a smaller car or carpooling works until congestion, rising fuel costs, or maintenance bills erode gains. If commuting time increases, stress spikes, or monthly transport expenses stop dropping, that’s a sign the car-centric strategy needs replacing.

Upgrade by diversifying transport options: season tickets or travelcards for rail, a mixed-modal routine combining cycling and public transport, or switching to a subscription-based car service for occasional needs. Factor in the value of time and wellbeing; sometimes paying a little more for a faster, less stressful commute is a net saving in productivity and health.

When DIY Repairs Create Recurring Costs — Replace Quick-Fix Mindsets

Do‑it‑yourself repairs save money until they don’t. Frequent re‑repairs, botched fixes or warranty voidance are clear signs your DIY approach is costing you more in the long term. If you’re repeatedly touching the same problem, the real cost is time and escalating damage.

Replace piecemeal fixes with preventive maintenance and selective professional help. Schedule annual checks for plumbing, roofing and heating systems; invest in a trusted tradesperson for warranty-safe repairs. Pay a bit now to avoid compounding costs and regain predictable monthly outlays.

When Your Insurance Savings Leave You Underinsured — Replace Cheap Policies

Switching insurers to shave premiums is a common monthly saving. The red flag that it’s time to replace this tactic is discovering gaps when you need to claim—or facing surging premiums after a single payout. Being underinsured is a brittle saving that can collapse with one incident.

Upgrade by reviewing cover levels and excesses annually, bundling sensibly, and choosing providers with reliable claims records rather than the lowest sticker price. Sometimes paying a higher premium reduces risk and volatility in your monthly finances.

When Bank Fee Avoidance Becomes Risky — Replace the Bare‑Minimum Account

Avoiding bank fees by using niche accounts or cash‑heavy strategies can be smart, but warning signs include limited access to credit, poor interest rates on savings, or failed fraud protections. If your banking choices hinder major purchases, mortgage approval, or leave you exposed to scams, the bargain accounts are no longer fit for purpose.

Replace bare‑minimum accounts with a balanced banking setup: a high‑interest savings account, a current account with decent fraud protection and an automatic bill‑payment buffer. Consider credit-builder products if you need a healthier credit profile; the monthly premium is often outweighed by long-term borrowing savings.

When Tech and Gadgets Turn into Time Sinks — Replace ‘Cheap Device’ Thinking

Buying the cheapest devices or using outdated tech to save money is practical until software incompatibility, poor battery life or security issues begin to drain value. If updates stop, apps lag, or repair costs accumulate, the initial savings have been eroded.

Upgrade selectively: invest in fewer, higher‑quality devices that last longer and receive updates, or switch to refurbished models from reputable sellers with warranty. Factor in productivity gains: a reliable laptop or smartphone can be a monthly saver in time and frustration.

When Small Side Hustles Stall — Replace One-Off Gigging with Scalable Income

Picking up occasional gigs is a go-to for extra monthly cash, but a clear sign it needs upgrading is income volatility, burnout, or an inability to scale beyond a few hours a week. If the work consumes weekend time without appreciable financial progress, the tactic has limited upside.

Replace ad-hoc hustling with scalable income streams: build repeatable freelance packages, create digital products, or invest time in skills that command higher rates. Automate where possible—templates, outsourcing and passive components—so the monthly benefit grows without equivalent increases in time invested.

When Your Savings Strategy Lacks a Feedback Loop — Replace Static Budgets

Many people adopt a monthly budget and stick to it, believing discipline alone will yield results. The sign that this needs replacing is a budget that remains unchanged year after year despite shifting priorities, inflation, life events or goals. Static budgets calcify good habits but blind you to new opportunities.

Upgrade to a dynamic savings system: quarterly goal reviews, rolling allocations that respond to life changes, and an annual rebalancing of priorities (housing, investments, experiences). Use automated transfers to savings and investment accounts, but regularly examine whether those transfers match your current objectives. The best saving method is the one that evolves with you.

![Como viver com menos do que você ganha [sem se sentir miserável]](https://productivepathblog.com/wp-content/uploads/2026/05/How-to-Live-Frugally-PTqOcG-559x1024.jpg)