Why ask the experts — and what they won’t tell you in listicles

Most ’10 ways to save’ articles stitch together obvious tips. Experts, however, approach saving as a craft: they diagnose the person before prescribing tactics. A chartered financial planner will prioritise cash flow architecture; a behavioural scientist looks at decision friction and habits; an energy consultant maps the home’s thermodynamic profile. That means the same ten tactics look very different depending on diagnostics. In short: context matters. The expert’s first step is rarely “cancel your subscriptions” — it’s “what problem are the subscriptions solving?”

This section reframes the rest of the piece: these aren’t ten isolated tactics but ten expert lenses. Read them as diagnostic tools you can apply to your own finances rather than rote rules to follow.

1. The planner’s reallocations: optimise before you cut

Financial planners urge clients to treat saving like portfolio management. Instead of brute-force trimming, they reallocate: move tax-efficient contributions (pension or ISA) to the front of the month, automate employer-matching pension top-ups, and prioritise high-interest debt repayment. That reduces waste while preserving lifestyle.

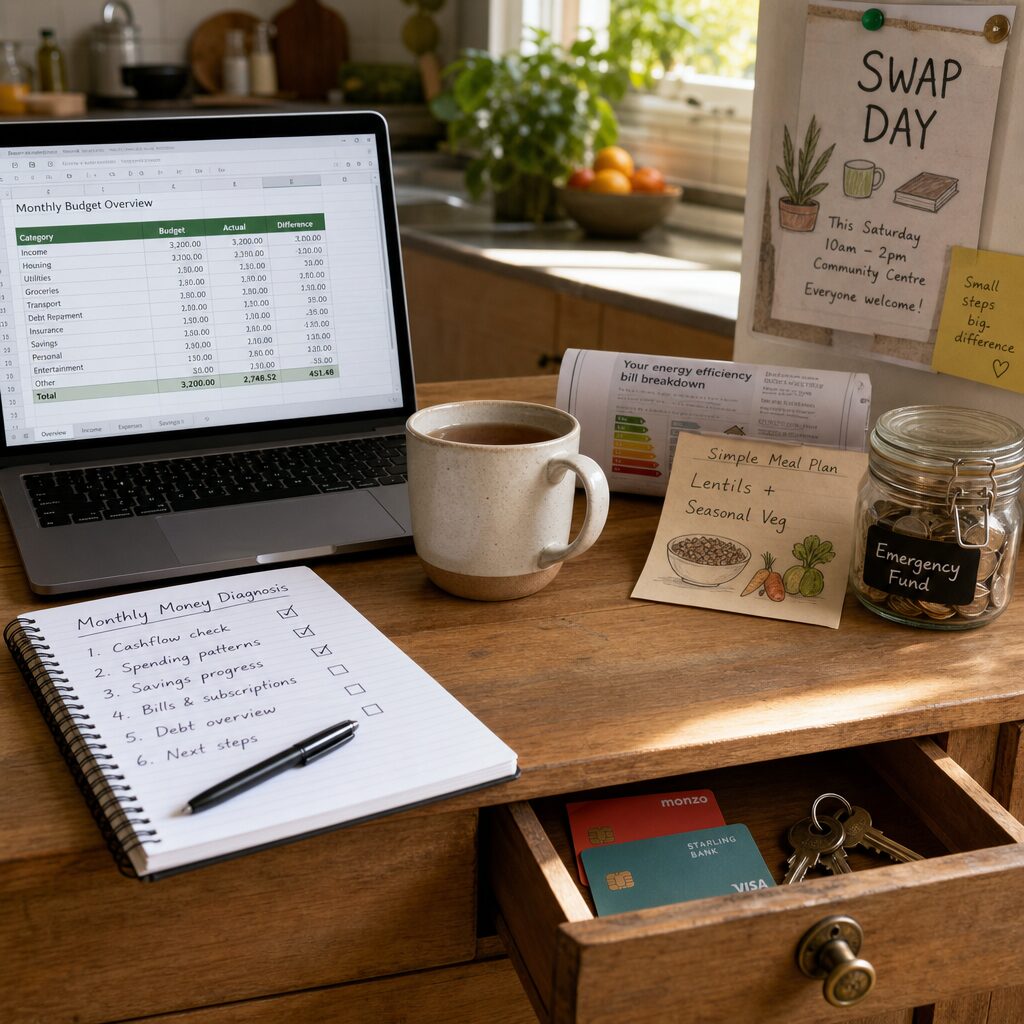

A planner’s practical monthly checklist: automate savings transfers on pay day; funnel windfalls (bonuses, tax refunds) into a separate rainy-day account; and set a target micro-goal (e.g. add £50 to emergency savings each month) to create momentum. The expert advantage is using structure to make saving painless rather than punishing.

2. The behavioural scientist’s nudge: change the environment, not the willpower

Behavioural scientists emphasise altering choice architecture. The trick isn’t telling you to be disciplined; it’s making poor choices harder and good choices automatic. Practical moves include: move your credit card to a locked drawer and use a debit card for daily spend; delete shopping apps or remove saved payment details; set a one-click rule for recurring purchases.

They also recommend ‘implementation intentions’ — very specific plans like “If I feel the urge to buy non-essential clothing, I will wait 72 hours and check my budget app.” Small frictions and time buffers reduce impulsive spend without creating deprivation.

3. The energy consultant’s micro-investments: insulate to save

Energy consultants point out that monthly savings often grow from one-off micro-investments. Draught-proofing, pipe lagging, and upgrading to LED downlights can cut monthly bills noticeably. They advise prioritising measures with the quickest payback: thermostatic radiator valves, smart thermostats calibrated properly, and simple loft insulation top-ups.

Their rule of thumb: target measures with a payback under three years first. Unlike subscription cuts, these changes reduce recurring outgoings while increasing home comfort — a psychological double win that sustains the behaviour.

4. The negotiator’s secret: ask like a pro, switch like a winner

Customer retention teams know how to keep you paying; negotiators teach you how to extract value. Experts recommend a monthly habit of negotiating at least one bill: broadband, mobile, or insurance. Prepare: know competitor offers, note how long you’ve been a customer, and ask for the retention or loyalty department.

If negotiation fails, switching is often superior. Use price-comparison windows (e.g. energy and broadband) to force providers’ best offers. Professionals set calendar reminders to review critical contracts annually — small repeated wins compound into significant savings.

5. The dietitian and frugal cook’s approach: planning that saves calories and cash

Nutritionists who work with tight budgets design meal patterns to reduce food waste and cost-per-meal. Their tenets: batch cook, repurpose leftovers, embrace legumes and frozen veg, and build a rotating shopping list of staple deals. They also advise planning meals around in-season produce and supermarket promotions, not temptation-led aisles.

A concrete monthly tactic: pick two ‘theme weeks’ each month (for example, ‘stews and soups’ in winter) and shift more expensive proteins to once a week. That reduces grocery bills and simplifies shopping — both powerful levers for sustained savings.

6. The tax adviser’s overlooked moves: small timing, big returns

Tax advisers highlight timing and structure as underused savings levers. Adjusting the timing of pension contributions, utilising annual ISA allowances before the tax year-end, and claiming eligible work-from-home expenses can alter your effective disposable income. These are not glamorous, but they legally improve after-tax cash flow.

Professionals suggest an end-of-quarter check: have you used your ISA allowance? Are you maximising employer benefits? Often a one-hour review with a tax adviser or an informed DIY audit yields recurring monthly improvements through better tax efficiency.

7. The psychologist’s framing: switch from ‘saving’ to ‘earning peace’

Psychologists argue that people stick to financial habits when they’re framed positively. Instead of mentally shaving budgets, frame changes as ‘buying security’ or ‘making room for experiences.’ This reframing increases intrinsic motivation and reduces the sense of sacrifice.

Practically, create a visual cue: a labelled savings jar or a dedicated app goal showing what the saved money will enable (holiday, course, debt-free month). The emotional reward of progress — not the spreadsheet — is what sustains monthly savings.

8. The small-business owner’s hustle: monetise skills, not time

Entrepreneurs focus on diversified income streams rather than extreme cutting. Experts advise finding one small monetisable skill you can scale for a few hours a month: teach a mini-class, freelance on weekends, rent out space or equipment. Even modest additional income earmarked for savings accelerates net-monthly gains.

The practical formula many pros use: pick a low-friction side income, automate 100% of its proceeds to a dedicated savings pot, and review scalability every quarter. It’s less painful to save money you didn’t psychologically count as ‘lost spending’.

9. The tech lead’s stack: let software babysit your budget

Tech experts harness automation beyond standing orders. They use rules in banking apps to round up transactions into savings, set multiple targeted savings pots, and automate bill-splitting to avoid disputed payments. They also audit app permissions to prevent accidental subscriptions.

Adopt the tech lead habit: schedule a monthly 15-minute ‘finance hygiene’ session — clear unused digital subscriptions, adjust automated rules, and reconcile surprise charges. Small, regular maintenance keeps leakage minimal.

10. The community organiser’s multiplier: swap, share and co‑operate

Community organisers see saving as a social activity. Carpooling, tool libraries, clothing swaps, and skill swaps reduce individual costs and build social capital. These solutions often replace recurring expenses (gardening services, maintenance tools) with collaborative alternatives.

Start small: join a local swap group or community garden, host a clothes-swap once a season, or use neighbourhood apps to borrow seldom-used items. The financial gain is steady; the social benefit often makes the changes stick.

Putting the experts together: an action sheet for the month

Combine lenses: run a one-hour diagnosis this month. Step 1: checklist from the planner (automate savings). Step 2: apply one behavioural nudge (remove saved cards). Step 3: book one micro-investment (draught-proof a window). Step 4: negotiate one bill. Step 5: plan your weekly meals around two theme weeks. Step 6: check ISAs/pensions. Step 7: reframe a goal and visualise it. Step 8: pick a small side income. Step 9: automate tech rules. Step 10: join one community swap.

Experts don’t promise overnight riches. Their advice compounds: small, diagnostic-led changes, repeated monthly, lead to substantial annual results. The advantage of the expert approach is the mixture of mindset, one-off investments and systems — a practical blueprint for sustainable saving.

Final thought: measure what matters

Professionals measure outcomes, not intentions. Track three metrics monthly: net cash saved, recurring outgoings reduced, and one-off payback progress (insulation, thermostat, debt repayment). Use these to iterate next month’s plan.

Saving is not a moral test; it’s a behaviour to design. Treat it like an experiment guided by experts’ diagnostic lenses and you’ll be surprised how much monthly saving can be achieved without living miserably.

![Como viver com menos do que você ganha [sem se sentir miserável]](https://productivepathblog.com/wp-content/uploads/2026/05/How-to-Live-Frugally-PTqOcG-559x1024.jpg)