When saving hacks become financial antiques

Every frugal strategy has a shelf life. What began as a clever monthly routine can calcify into habit without thought, draining time or even money. This section explains why it pays to audit not just your accounts but the saving strategies themselves.

Think of your money habits like a small-business product line: some offerings outperform and deserve scaling, others slow down and require discontinuation. The key is to spot objective signs — diminishing returns, rising friction, or lifestyle mismatch — that indicate a tactic has become an expense rather than a saving.

1. Shopping with coupons: signs it’s time to retire the coupon clip

Coupons once shaved real pounds off your weekly shop, but signs it’s time to replace this tactic include spending more time chasing deals than you save, buying unnecessary items because they’re discounted, or noticing that the real prices have risen to offset promotions.

If the cognitive load of couponing (sorting, expiry dates, stacking rules) outweighs the savings, consider automated price-tracking apps or bulk-buying staples on a schedule. These modern replacements reduce effort while preserving savings.

2. DIY home repairs: when patched pipes cost more than professionals

DIY used to be the go-to money-saver, but repeated fixes that fail to solve the root cause are a tell-tale sign it’s time to upgrade. If your temporary repairs keep recurring, if you’ve caused damage that later required professional correction, or if the time you spend researching and executing projects eats into paid work, it’s time to rethink the approach.

Switching to preventative maintenance plans, scheduled professional inspections, or investing in higher-quality tools/services can save money over time and protect your home’s value.

3. Cutting utilities aggressively: when sacrifice becomes unhealthy

Turning off heaters, reducing hot water use, or dialing down electricity can be frugal — until comfort or health suffers. Signs to stop include family complaints, increased illness, or appliance overuse leading to breakdowns. There’s also a tipping point where the inconvenience prompts wasteful workarounds (space heaters, frequent laundering) that raise costs.

Upgrade by investing in efficiency: improved insulation, smart thermostats, or energy-efficient appliances. These require upfront spend but reduce bills sustainably and keep quality of life intact.

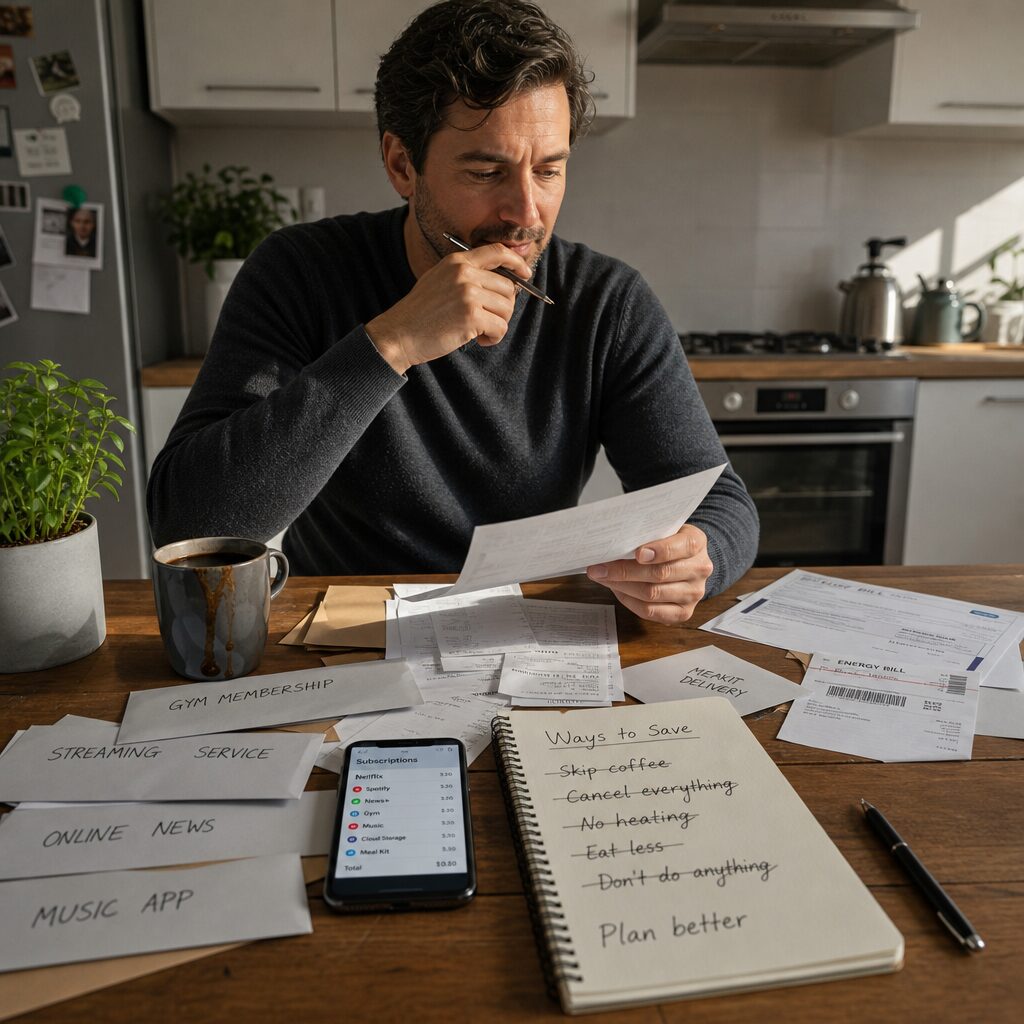

4. Minimal subscriptions: when the saving becomes a scramble

Trimming subscriptions is low-hanging fruit, but constant subscription hopping or cancelling and resubscribing to chase promotional rates is a sign of diminishing returns. If you’re losing access to services you rely on, encountering repeated administrative friction, or spending hours managing billing cycles, the method has become inefficient.

Consider consolidating to family plans, annual payments for lower effective rates, or negotiating directly with providers. A well-chosen subscription can be a net time and money saver.

5. Strict meal-prep regimes: when food savings spoil social life

Meal-prepping saves cash, yet rigid plans that exclude spontaneity, lead to food fatigue, or cause wasted perishable items signal it’s time to evolve. If you’re declining social invitations because of meal planning or frequently throwing out unused prepped meals, the savings are hollow.

Adopt flexible meal strategies: batch-cook versatile components, freeze portions, or use meal-kit discounts occasionally. These adjustments enhance enjoyment and reduce waste while keeping costs down.

6. Public transport only: when time is the hidden cost

Relying solely on public transport makes sense financially, but long commutes, poor reliability, or the inability to reach opportunistic jobs or gigs are signals to reassess. Time is money; if delayed trains cost you work or opportunities, the apparent saving is a liability.

Consider hybrid approaches: occasional car hire, cycle-to-work options, or flexible work arrangements that balance cost with opportunity. Evaluate the hourly value of your time when making the trade-off.

7. Extreme sale shopping: when fashion savings erode your wardrobe

Hunting sales for clothing feels thrifty until you’re left with a wardrobe of ill-fitting, low-quality items that wear out quickly. Signs to replace this tactic include frequent replacements, increased laundering or repair costs, or embarrassment at work or social events.

Shift to a quality-over-quantity approach: invest in fewer, durable wardrobe pieces, use capsule strategies, and buy off-season at trusted retailers. The per-wear cost falls, and you save money and time choosing outfits.

8. Avoiding financial advice: when self-guided thrift becomes risky

Doing your own financial housekeeping is admirable, but persistent uncertainty, missed tax optimisation, or fear of investing are indicators it’s time to seek professional help. If you’re consistently underperforming low-cost benchmarks or ignoring complex areas (retirement planning, tax-efficiency), the DIY route may cost you dearly in the long term.

Upgrade by consulting a regulated adviser for a health check, using robo-advice for low-cost portfolios, or attending financial workshops. Small professional investments often multiply savings and reduce costly mistakes.

9. Cash-only budgeting: when envelope systems constrain growth

The envelope system or strict cash-only methods discipline spending, but signs it’s time to replace them include missing out on digital rewards, poor record-keeping for taxes, or logistic friction in an increasingly cashless world. If you’re paying more in fees or losing cashback and credit-building opportunities, the method is outdated.

Modernise with hybrid systems: use prepaid cards for categories, automated transfers to savings pots, or apps that replicate envelope rules digitally while capturing rewards and transaction data.

10. Free entertainment only: when frugality isolates you

Choosing only free entertainment can keep budgets tight, but if you withdraw from social life, miss cultural experiences, or experience boredom that leads to impulse spending, the tactic backfires. Signs include reduced social invitations, stagnating personal growth, or impulsive splurges to break monotony.

Trade absolute frugality for curated experiences: allocate a modest ‘social fund’ monthly, prioritise high-value activities, and seek community discounts or memberships that enrich life without overspending.

How to replace a worn-out tactic: a five-step refresh plan

Recognising a tactic is the first step; replacing it requires a plan. Begin with an audit: quantify time, money and stress costs for each method. Next, rank tactics by return-on-investment and friction.

Third, pilot replacements on a small scale: switch one method at a time and measure impact for two months. Fourth, automate the successful replacements to remove human error and temptation. Finally, iterate annually — habits age, markets change, and periodic refreshes keep your monthly savings smart, scalable and aligned with your life.

Conclusion: treat your savings strategy like a living system

The smartest way to save every month is not rigid thrift but adaptive stewardship. Watch for clear signs — rising effort, declining returns, deteriorating quality of life — and be willing to upgrade. Small, timely investments in efficiency, quality or advice often restore and amplify savings more reliably than stubbornly clinging to outmoded hacks.

Make a yearly habit of reviewing your top saving techniques and consider replacement not as failure but as evolution: your future self will thank you.

![Como viver com menos do que você ganha [sem se sentir miserável]](https://productivepathblog.com/wp-content/uploads/2026/05/How-to-Live-Frugally-PTqOcG-559x1024.jpg)